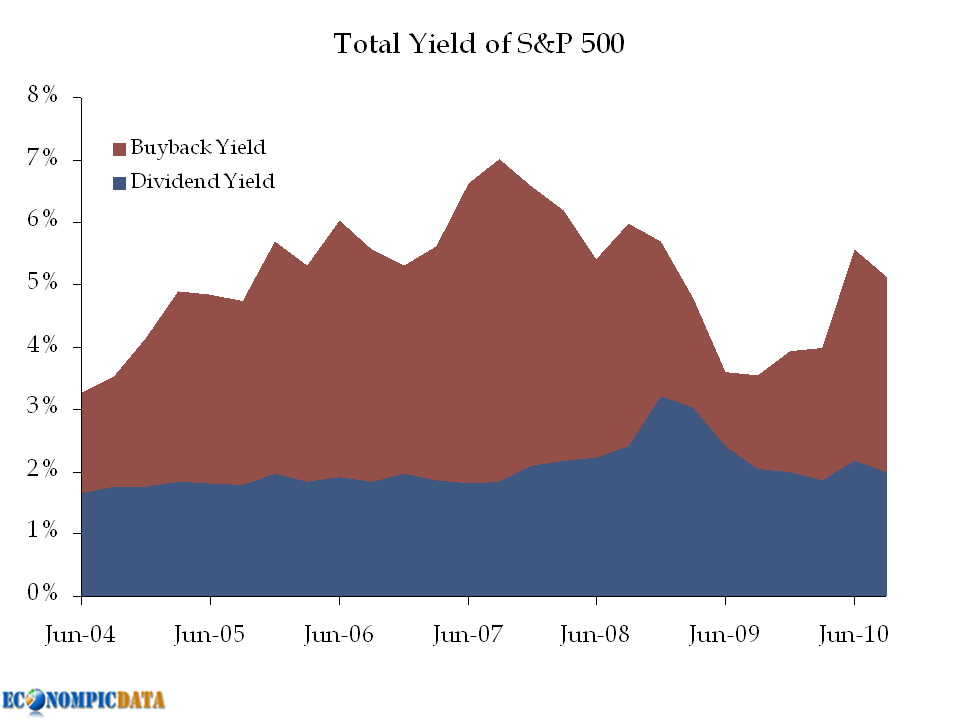

S&P's most recent update indicates that US companies, after a pause for about a year after the banking crisis, are back in the buyback game. In the third quarter of 2010, the S&P 500 companies bought back almost $ 80 billion of stock, up 128% from the third quarter of 2009.The below chart shows the dividend yield (dividends divided by the S&P 500's market cap) and buyback yield (buybacks divided by the S&P 500's market cap) on a quarterly basis (annualized) going back to 2004.

While getting cash back to shareholders is the whole point of investing in stocks (timing of returning that cash is potentially a broader question), the higher buyback yield is not necessarily a great thing; it is a great thing if the cash is buying back stock when cheap... not when expensive. And when were corporations buying back the most? Q2 and Q3 2007 (i.e. the market peak). The lowest? Q1 and Q2 2009 (i.e. the market trough).

Professor Damodaran does provide some rationale / discussion into why the trend has moved to buyback vs. dividend:

- Manager compensation: buybacks increase the price of stock for manager option grants

- Uncertainty about earnings: buybacks are a lot more flexible than a steady dividend

- Changing investor profiles: investors that are more focused on stock price

- Higher earnings per share: less shares outstanding = more earnings per share

{kind=link}

{kind=link}